The Citizen Petition for Audit is a system where, in accordance with Article 242 of the Local Autonomy Law, an citizen petitions for an audit to the Audit and Inspection Commissioners and requests them to examine the financial affairs of the Metropolitan Government and, if necessary, to take appropriate measures.

The purpose of this system is to ensure the proper management of Metropolitan Government finances and to protect the interests of all Tokyo residents, by performing audits based on requests from the residents themselves.

Instead of an audit by Audit and Inspection Commissioners, the citizen may instead choose to request an audit by an external auditor (for which a CPA, lawyer, and certain other persons may be qualified).

An audit by an external auditor will be performed when the Audit and Inspection Commissioners deem it necessary, the assembly approves it, and the governor concludes a contract for an individual external audit with the said auditor.

The scope of this audit is limited to the financial affairs of the Metropolitan Government, details of which are listed below

1 to 4 above includes such cases when the conduct in question can be estimated with a high degree of certainty.

If one year or more has passed since the act in question was conducted however, without due reason, the request will be rejected.

A person who is registered as residing at a Tokyo address is able to submit a request for an audit.

A corporation that has a Tokyo registered address is also qualified to petition for an audit.

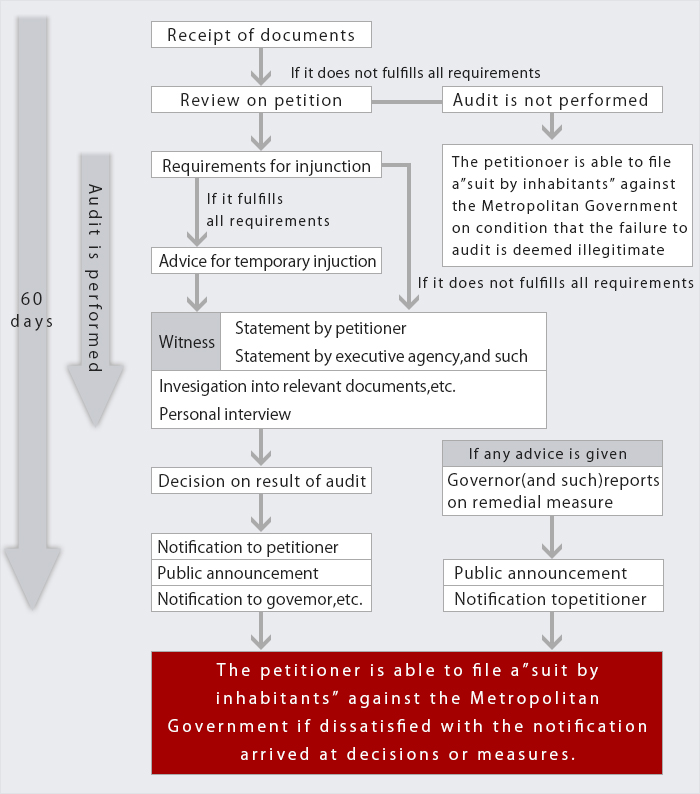

In the case of an audit by Audit and Inspection Commissioners, the workflow after receiving the petition is as follows:

Note

1. A petition is reviewed to ascertain whether or not the act subject to the audit request falls under financial affairs of the Metropolitan Government, whether or not the address of petitioner fulfills the domicile requirement, and such.

2. A judgment not to perform an audit corresponds to a “rejection” in a lawsuit.

3. The period to file a suit by citizen is limited (under Article 242-2 of the Local Autonomy Law).

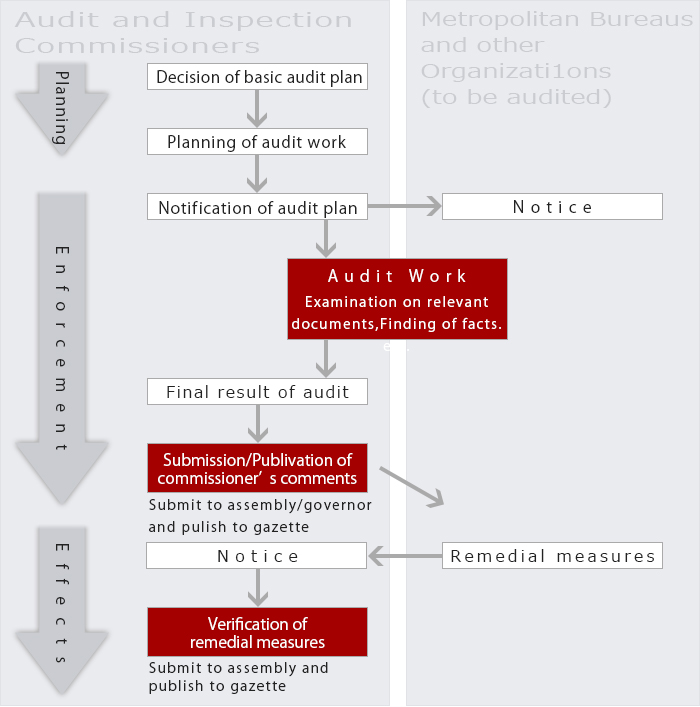

In the case of an audit by external auditor, the workflow after receiving the petition is as follows:

Please see our web page (JAPANESE).(Official correspondence shall be made inJapanese only.)

Link to Guide on "How to Submit a Request of Audit" (JAPANESE)